Jerry Sandusky convicted and sentenced to life on 45 counts of child sexual abuse

President Obama re-elected

NFL replacement refs fuck up Green Bay/Seattle game

Christopher Stevens killed in embassy attack in Libya over anti-Muslim video

Gunman opens fire at theater in Aurora Colorado killing 12 and wounding over 50

Gunman opens fire at Sikh temple in Milwaukee WI killing six and wounding four.

Hurricane Sandy

David Petraeus resigns as Director of CIA over his affair with Paula Broadwell

Whitney Houston dies of drug overdose

GOP war on women

Kansas City Chiefs player Javon Belcher murders girlfriend, then commits suicide at team headquarters

Gunman opens fire at Sandy Hook grade school, killing 20 students, six teachers, his mother, then himself.

RIP in 2012

Etta James

Sarah Burke January 19

Joe Paterno January 22

Whitney Houston February 11

Davy Jones February 29

Andrew Brietbart March 1

Mike Wallace April 7

Dick Clark April 18

Junior Seau May 2

Vidal Sasson May 9

Donna Summer May 17

Robin Gibb May 20

Richard Dawson June 2

Rodney King June 17

Andy Griffith July 3

Sage Stallone July 13

Kitty Wells July 16

Sally Ride July 23

Sherman Hemsley July 24

Tony Martin July 27

Gore Vidal July 31

Acott McKenzie Aug 18

Phyllis Diller Aug 20

Neil Armstrong Aug 25

Art Modell Sept 6

Andy Williams Sept 26

Alex Karras Oct 10

George McGovern Oct 21

Russell Means Oct 22

Larry Hagman November 23

Zig Ziglar November 28

Javon Belcher December 1

Jerry Brown December 8

Sarah Burke January 19

Joe Paterno January 22

Whitney Houston February 11

Davy Jones February 29

Andrew Brietbart March 1

Mike Wallace April 7

Dick Clark April 18

Junior Seau May 2

Vidal Sasson May 9

Donna Summer May 17

Robin Gibb May 20

Richard Dawson June 2

Rodney King June 17

Andy Griffith July 3

Sage Stallone July 13

Kitty Wells July 16

Sally Ride July 23

Sherman Hemsley July 24

Tony Martin July 27

Gore Vidal July 31

Acott McKenzie Aug 18

Phyllis Diller Aug 20

Neil Armstrong Aug 25

Art Modell Sept 6

Andy Williams Sept 26

Alex Karras Oct 10

George McGovern Oct 21

Russell Means Oct 22

Larry Hagman November 23

Zig Ziglar November 28

Javon Belcher December 1

Jerry Brown December 8

Prudential Financial PRU stock prediction 2013

Prudential Financial PRU stock prediction 2013 ; Prudential Financial Inc. (PRU), the second-largest life insurer in the U.S., said it expected to earn between $7.50 and $7.90 a share next year, an increase over 2012, driven in part by growth in existing units and the completion of previously announced deals.

Analysts polled by Thomson Reuters had been predicting operating earnings per share of $7.88 next year on average. Prudential has earned $4.43 per share through the first nine months of 2012 and analysts so far expect $1.75 in the fourth quarter. The earnings guidance was disclosed in a slideshow included in a regulatory filing in advance of Prudential's third-quarter conference call, where executives plan to discuss their outlook for 2013.

The company, which announced a 10% dividend increase, said it would end the year with "readily deployable capital" of $1.2 billion to $1.5 billion. Share buybacks were one driver of 2013 earnings growth listed by the company in the slides. Prudential also predicted operating return on equity, another measure of profitability, would rise to 12.2% to 12.8% in 2013.

The company's operating return on equity was 10.2% through the first nine months of this year. The earnings-per-share outlook for next year assumes that interest rates, which have damped returns in investment portfolios across the insurance industry, will stay low. It also assumes the company will complete a previously announced acquisition of a life-insurance business from Hartford Financial Services Group Inc. (HIG) in the first quarter and a large pension transaction in the fourth.

The tentative model also predicted the price would grow in the first half of 2012 to $52. Therefore, we foresaw a negative correction in March-April. The actual price started to fall in the beginning of May and the monthly closing price for May was at the level of $45 per share. The updated model, as obtained with new data between March and October 2012, predicts a healthy growth in the price in 2012Q4. In January 2013, the price may reach the level of $64. On November 20, the closing price was $50.78. There is some potential of a 10% to 15% return at a three month horizon. One may consider PRU as an investment idea at this horizon.

The model has been obtained using our concept of share pricing as a decomposition of a share price into a weighted sum of two consumer price indices. The intuition is clear - there is a set of goods and services which any company produces and this set defines the share price evolution of a given company relative to other companies.

These other companies are also driven by prices for some goods and services. Hence, for a given company one needs two defining sets of goods and services to estimate its relative pricing power - one related and one as an independent reference. Thus, the relevant stock price can be defined by two CPIs which include corresponding goods and services.

Many SA readers have reasonable doubts that some consumer price, which is not directly related to goods and services produced by a given company, may affect its price. We allow the economy to be a more complex system than described by a number of simple linear relations between share prices and goods. The connection between a firm and its products may be better expressed by goods and services which the company does not produce or provide. The demand/supply balance is fragile and may evolve along many nonlinear paths. It would be too simplistic to directly define a company price only by its own products.

Originally, we addressed the PRU model in 2009 and found two CPIs explaining the monthly closing prices of PRU since 2003. They were the consumer price index of food and beverages (F) and the index of transportation services (TS). The defining time lags were as follows: the food index led the share price by 5 months and the TS index led by 4 months:

PRU(t) = -6.09F(t-5) - 3.15TS(t-4) + 59.76(t-1990) + 930.50, September 2009

In 2010 and 2012, we revisited the original model and estimated new coefficients and lags. These estimates were close to the original ones:

PRU(t) = -5.45F(t-5) - 3.98TS(t-3) + 59.66(t-1990) + 1055.38, September 2010

PRU(t) = -5.14F(t-5) - 3.80TS(t-4) + 56.20(t-1990) + 1005.63, February 2012

Here we revisit the model. We have borrowed the time series of monthly closing prices of PRU from Yahoo.com and the relevant (seasonally not adjusted) CPI estimates through October 2012 are published by the BLS. The best-fit model for PRU(t) is as follows:

PRU(t) = -5.09F(t-5) - 3.67TS(t-3) + 55.44(t-2000) + 1531.31, October 2012

where PRU(t) is the PRU share price in U.S. dollars, t is calendar time. One can conclude that the model has not been changing since January 2009 and thus provides a good estimate of the price at a three month horizon.

Figure 1 displays the evolution of both defining indices since 2002.

Figure 2 depicts the high and low monthly prices for a share together with the predicted and measured monthly closing prices (adjusted for dividends and splits). The predicted prices are well within the limits of the high/low share price which might be considered as the actual price uncertainty.

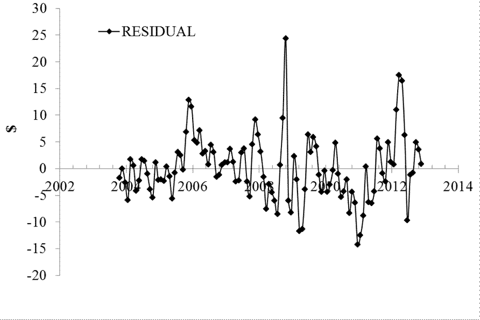

The model residual error is shown in Figure 3 with the standard deviation between July 2003 and October 2012 of $6.01 ($5.58 in March 2012).

Source ref:

http://online.wsj.com?mod=djnwires

http://seekingalpha.com/article/1024801-prudential-financial-may-rise-to-64-in-january-2013

pru shares prices 2013, pru stock prediction 2013, pru eps estimates 2013, pru earnings per share 2013, earnings-per-share outlook for next year

Market Research Australia Insurance Report 2013

Market Research Australia Insurance Report 2013 ; As was the case in our 2012 Annual Report, it is the strengths of Australia's insurance sector that stand out. In most countries, wealth management is an ancilliary activity that is undertaken by life insurers or commercial banks. In Australia, the development over nearly 30 years of the superannuation (pension) fund industry means that wealth management is a core business. Moreover, the superannuation funds, with their roughly AUD1,400bn in assets under management (AUM) continue to grow. They are fed in part by contributions from employers on behalf of employees that are determined by the Superannuation Guarantee (SG) Levy rate. Currently 9% of employees' income, this will rise to 12% by mid-2019.

In the short-term, though, the insurers are responding to a number of changes that have been imposed by the regulator and the Treasury. APRA's Life and General Insurance Capital framework will become effective from the beginning of 2013. Broadly analogous to Solvency II in Europe, it has required all insurers to implement some operational changes. However, both the non-life and the life companies are well capitalised and will be able to cope. For the life insurers, the Stronger Super and the Future of Financial Advice (FoFA) reforms will intensify the downwards pressure on fees and prices. However, over the longer term, they will probably improve the perceptions of the insurance/ wealth management industry in Australia of consumers/investors.

In the recent past, the leading life insurers have been consolidating already strong market positions by exploiting brands or making acquisitions that reinforce their offerings in particular, usually quite rapidly growing areas. Foreign life groups are competing in Australia, but are tending to focus on niches where brand and (established, multiple) distribution channels are less important.

Australia's world-class non-life companies were heavily exposed to natural catastrophes in Australia, New Zealand and elsewhere in early 2011. Given their broad portfolios, they have since been exposed to higher reinsurance costs. However, almost all the non-life companies have been able to achieve (near) double-digit premium growth in H112 relative to H111. Combined operating ratios have generally improved quite dramatically, in part because of the strengthening in prices and rates and in part because of lower claims. Underwriting has been characterised by discipline in a market that is competitive, but which is sufficiently large that a number of players can focus on profitable niches. Meanwhile, QBE, Australia's leading multi-national insurer, continues its overseas expansion by way of acquisition. IAG, for its part, has already developed a substantial commercial footprint elsewhere in the Asia-Pacific. View Full Report Details and Table of Contents

About Fast Market Research

Fast Market Research is an online aggregator and distributor of market research and business information. Representing the world's top research publishers and analysts, we provide quick and easy access to the best competitive intelligence available. Our unbiased, expert staff will help you find the right research to fit your requirements and your budget. For more information about these or related research reports, please visit our website at http://www.fastmr.com or call us at 1.800.844.8156.

U.S. Title Insurance industry outlook 2013 by Fitch Ratings

Best Insurance Stock - U.S. Title Insurance industry outlook 2013 by Fitch Ratings : Fitch Ratings maintained its stable rating outlook on the U.S. Title Insurance industry. The outlook reflects a belief that rating actions for the industry will on balance approximate current levels over the next 12 - 18 months as financial performance has improved recently and capital levels remain adequate based on several measures.

A new special report '2013 Outlook: U.S. Title Insurance Industry.' published today highlights key factors affecting title insurer ratings, reviews financial performance in 2012, and assesses industry prospects for 2013.

Operating profit margins on a GAAP basis for Fitch's title universe rose to 10.3 percent in the first nine months of 2012 versus 6.1 percent in the prior year. Earnings improved for all underwriters, but larger players First American Financial (FAF) and Fidelity National Title (FNF) posted the highest margins. Title revenues through nine months 2012 increased by over 15 percent as refinancing activity exceeded expectations and housing markets stabilized. The period's 90.7 percent underwriting combined ratio reached levels unseen since 2006, as growth reduced expense ratios and claims experience improved as well.

The title insurance industry is benefitting from an improving housing market that is showing less home inventory and increasing home prices nationally. According to the National Association of Realtors (NAR), US housing prices rose in 2012 with many markets showing year-over-year home price growth for the first time since the beginning of the housing crisis. Economists attribute the price increase primarily to reduced housing inventory and, to a lesser extent, fewer homes sold in distress.

The Mortgage Bankers Association of America (MBA) forecasts mortgage originations to decline to $1.3 billion in 2013 and just over $1 billion in 2014, compared with $1.7 billion in 2012. The drop is driven by a projected material decline in refinance activity over the next two years, which is expected to be somewhat offset by greater purchase activity.

Fitch continues to view the industry as adequately capitalized, although individual company capital strength varies considerably. Fitch's view is based on both a non-risk adjusted approach such as net written premiums to surplus and a risk adjusted approach via Fitch's Risk Adjusted Capital (RAC) model.

The report '2013 Outlook: U.S. Title Insurance Industry' dated Nov. 26, is available at 'fitchratings.com' under 'Insurance' and 'Special Reports'.

Prospect Investing in Life Insurance Policies 2013

Best Insurance Stock - Prospect Investing in Life Insurance Policies 2013 , How Investing in Life Insurance Policy 2013 : Are you adequately insured ? Let this question be asked by every adult income-tax payer in his family. I would like every tax payer to take care of securing his family during the year against calamity. One of the best way to protect the family is to adequately insure all the family members.

It is time now for you not just to count your Life Insurance Policies for different members in the family but to sit down and ponder whether all the family members are adequately insured. In most cases I am sure the answer that will come in conclusion would be that most of the family members are not adequately insured.

Many people avoid investing in life insurance simply because they imagine the costs as being too high for their budgets. Fortunately, there are a wide variety of insurance policies available for every set of needs and budgets. Insurance providers provide death benefit payouts ranging from as little as a few thousand dollars all the way up to a few million. Most providers offer more affordable term life insurance policies—term policies have low premiums and payout death benefits for the duration of a specific period.

If low premiums aren’t a priority, the majority of life insurance providers feature coverage plans that accumulate cash value over the life of the policy. With universal and whole insurance it is possible to configure lucrative benefits packages that payout death benefits and can be cashed out or borrowed against like equity.

Hence, during the year 2013 please take a call to answer the question whether you and your family members are adequately insured. Do not forget to take an insurance policy for your dear loving daughter too.

What to Look for in a Life Insurance Policy

Policy Benefits

All insurance policies are different. We evaluated insurance providers largely on the variety and flexibility of the life insurance policies they offer. From five year term life insurance to variable universal policies, our leading picks for life insurance providers provide comprehensive coverage for every set of needs.

Pricing and Premiums

Premium payments are going to be different with different providers depending on risk factors such as your health, lifestyle, age and occupation. In general, insurance providers receiving a high score on our site gave more lucrative quotes than competitors regardless of age or lifestyle.

Additional Services

Life insurance is a must, but there are many other services we expect to see available in addition to, or as an alternative to, life insurance. Annuities, retirement planning, estate planning, mutual funds and plans tailored for small business are services we expect from the best providers.

Customer Support

Red tape and poor customer service are the last things a grieving family member wants to deal with. Our top picks for life insurance provider boast excellent customer service, approach claims in a timely and professional manner and go out of their way to meet customer expectations.

investment insurance 2013, investment insurance 2013, benefit investing insurance 2013, prospect investing in insurance 2013, life insurance investment products 2013, Prospect Investing in Life Insurance Policies 2013, equity investment life insurance company 2013

Travelers Companies (NYSE: TRV) stock rating by thestreet ratings

Best Insurance Tock - Travelers Companies stock rating by thestreet ratings : The Travelers Companies, Inc. (TRV) is a holding company. The Company, through its subsidiaries, is engaged in providing a range of commercial and personal property and casualty insurance products and services to businesses, Government units, associations and individuals., reiterated their buy rating on shares of The Travelers Companies (NYSE: TRV) in a research report sent to investors on Friday morning.

TRV has been the subject of a number of other recent research reports. Analysts at RBC Capital upgraded shares of The Travelers Companies from an outperform rating to a top pick rating in a research note to investors on Monday, December 17th. They now have a $87.00 price target on the stock, up previously from $85.00. Separately, analysts at Sanford C. Bernstein reiterated a market perform rating on shares of The Travelers Companies in a research note to investors on Thursday, December 6th. They now have a $77.00 price target on the stock. Finally, analysts at Zacks downgraded shares of The Travelers Companies from an outperform rating to a neutral rating in a research note to investors on Monday, November 26th. They now have a $75.00 price target on the stock.

The Travelers Companies traded down 0.17% on Friday, hitting $71.70. The Travelers Companies has a 1-year low of $55.86 and a 1-year high of $74.70. The stock’s 50-day moving average is currently $71.43. The company has a market cap of $27.350 billion and a price-to-earnings ratio of 10.25.

The Travelers Companies last announced its earnings results on Thursday, October 18th. The company reported $2.22 earnings per share for the quarter, beating the analysts’ consensus estimate of $1.54 by $0.68. The company’s quarterly revenue was up .4% on a year-over-year basis. On average, analysts predict that The Travelers Companies will post $5.53 earnings per share for the current fiscal year.

To view TheStreet’s full report, visit www.thestreetratings.com

Happy 4th or 5th Birthday Tripp Easton Johnston!

Who knows if Tripp was actually born on this day, he may have been born before December 28, January 2009, 2008, or 2007. Anyway today is his "official" birthday.

Happy Birthday Tripp! Hope daddy, Sunny, Breeze, Grandma Sherry and Auntie Sadie got to spend time with you. But I'm sure the Palin side wouldn't allow it.

Here are some more comparison pics of Levi, Trigg, and Tripp. Happy comparing!

Happy Birthday Tripp! Hope daddy, Sunny, Breeze, Grandma Sherry and Auntie Sadie got to spend time with you. But I'm sure the Palin side wouldn't allow it.

Here are some more comparison pics of Levi, Trigg, and Tripp. Happy comparing!

Dylvan Klovig and his relationship to the Palins

This is the only picture of Dylan I could find.

I don't know much about Klovig and the ship incident in Juneau. Can someone fill me in? Thanks. All I know is that he was a friend of Bristols.

W.R. Berkley insurance stock Rating prices target

Best Insurance Stock - W.R. Berkley insurance stock Rating prices target : Zacks reiterated their neutral rating on shares of W.R. Berkley (NYSE: WRB) in a research note issued to investors on Wednesday. The firm currently has a $41.00 target price on the stock.

Zacks’ analyst wrote, “Berkley posted third-quarter earnings ahead of the Zacks Consensus Estimates on the back of higher premium written, pricing gains, higher investment income and a lower share count. Year-to-date, the company has performed favorably and we expect the trend to continue. Berkley is witnessing stable retention and a general rate hike for the seventh consecutive quarter.

We believe that the insurance pricing cycle has entered a safe zone and the magnitude of the price rise will increase going forward. Berkley’s investments in a number of start-ups during the last four years will enable it to take greater advantage of the improved market scenario. Its International business is another area, which will fuel long-term earnings growth. A strong balance sheet and disciplined capital management are other positives. However, rising loss trends and a low interest rate environment keep us on the sidelines.”A number of other analysts have also recently weighed in on WRB. Analysts at Deutsche Bank cut their price target on shares of W.R. Berkley from $34.00 to $33.00 in a research note to investors on Monday, December 17th. They now have a sell rating on the stock. Separately, analysts at RBC Capital downgraded shares of W.R. Berkley from an outperform rating to a sector perform rating in a research note to investors on Monday, December 17th. They now have a $45.00 price target on the stock, up previously from $42.00. Finally, analysts at Goldman Sachs downgraded shares of W.R. Berkley from a neutral rating to a sell rating in a research note to investors on Tuesday, October 2nd. They now have a $35.00 price target on the stock. They noted that the move was a valuation call.

W.R. Berkley traded down 1.55% on Wednesday, hitting $38.00. W.R. Berkley has a 52-week low of $33.34 and a 52-week high of $40.39. The company has a market cap of $5.161 billion and a price-to-earnings ratio of 11.86.

W.R. Berkley last posted its quarterly earnings results on Monday, October 22nd. The company reported $0.61 earnings per share for the quarter, beating the analysts’ consensus estimate of $0.55 by $0.06. The company’s revenue for the quarter was up 11.0% on a year-over-year basis. On average, analysts predict that W.R. Berkley will post $2.49 earnings per share for the current fiscal year.

The company also recently announced a special dividend, which is scheduled for Monday, December 31st. Stockholders of record on Monday, December 24th will be paid a dividend of $1.00 per share. The ex-dividend date is Thursday, December 20th.

W. R. Berkley Corporation (W. R. Berkley) is an insurance holding company. The Company operates in five segments of the property casualty insurance business: Specialty, Regional, Alternative markets, Reinsurance and International.

W. R. Berkley stock prices target, W. R. Berkley stock rating neutral, zack Analysts W. R. Berkley stock rating, Analysts at Deutsche Bank,

HCC Insurance Ex-Dividend Date Scheduled for December 28, 2012

Best insurance stock - HCC Insurance Ex-Dividend Date Scheduled for December 28, 2012 : HCC Insurance Holdings, Inc. ( HCC ) has announced an ex-dividend date of December 28, 2012 and a cash dividend payment of $0.165 per share scheduled for January 16, 2013. Shareholders who purchased HCC stock prior to the ex-dividend date are eligible for the cash dividend payment. This represents an 6.45% increase over the same period a year ago. At the current stock price of $37.24, the dividend yield is 1.77%.

The previous trading day's last sale of HCC was $37.24, representing a -1.09% decrease from the 52 week high of $37.65 and a 39.89% increase over the 52 week low of $26.62.

HCC is a part of the Finance sector, which includes companies such as American International Group, Inc. ( AIG ) and The Travelers Companies, Inc. ( TRV ). HCC's current earnings per share, an indicator of a company's profitability, is $3.5. Zacks Investment Research reports HCC's forecasted earnings growth in 2012 as 31.07%, compared to an industry average of 5.8%.

AIG Insurance stock prices prediction 2013

AIG Insurance stock prediction 2013 : American International Group, Inc. (AIG) is a leading international insurance organization serving customers in more than 130 countries. AIG companies serve commercial, institutional and individual customers through one of the most extensive worldwide property-casualty networks of any insurer. In addition, AIG companies are leading providers of life insurance and retirement services in the United States. AIG Common Stock, par value $2.50 per share (AIG Common Stock), is listed on the New York Stock Exchange, as well as the stock exchanges in Ireland and Tokyo.

AIG is an insurance conglomerate that spans the globe, but during the great recession like many other giant financial institutions, AIG got itself into a lot of trouble taking on the counter-party risk of mortgage backed securities. During the 4th quarter of 2008, AIG set the world record for reporting the biggest loss. It lost $99.3 billion dollars in a single quarter.

The company currently operates one of the largest insurance networks in the world, with more than 85 million clients in 130 countries. AIG is split into four business divisions: Chartis, SunAmerica Financial Group, Aircraft Leasing, and other operations.

Chartis offers a unique portfolio of insurance products and services. The insurance products are: casualty, property, financial lines, and specialty. Chartis conducts its business through multiple entities such as: New Hampshire Insurance Company, American Home Assurance Company, Lexington Insurance Company, AIU Insurance Company, Chartis Overseas, Fuji Fire & Marine Insurance Company Limited, Chartis Europe Holdings Limited, and Chartis Europe.

SunAmerica Financial Group - offers a comprehensive suite of products such as: term life, universal life, fixed/variable annuities, mutual funds, financial planning. The SunAmerica Financial Group operates under these subsidiaries: American General Life Companies (American General), Variable Annuity Life Insurance Company (Western National), SunAmerica Retirement Markets (SARM).

AIG's other operations primarily consisted of derivatives trading, and aircraft leasing. The other operations: International Lease Finance Corporation, AIG Markets, United Guaranty Corporation, AIG Financial Products, and AIG Trading Group Inc.

Currently AIG generates 91% of its revenue through the SunAmerica Financial Group, and Chartis.

AIG's current management strategy remains simple: by 2015 achieve return on equity above 10%, generate share growth in mid-teens, grow insurance divisions, and reinvest retained earnings.

AIG aggressively competes with Berkshire Hathaway (BRK.A/BRK.B), The Travelers Companies (TRV), Chubb (CB), Allstate (ALL), Loews (L), Progressive (PGR), Hartford Financial Services (HIG), CNA Financial (CNA), among many others.

Technical Analysis AIG insurance 2013

The stock has been on a continuous up-trend since November 2012. On 12/24/2012 the stock is between a very narrow symmetrical triangle formation. I anticipate the stock to break out no later than the 26th or 27th, meaning that the stock will be forced to make a major move.

Source: Chart from freestockcharts.com

The stock is trading above the 20-, 50-, and 200- Day Moving Averages. The stock will experience further upside through 2013, as investors have under-bought the growth prospects of the company.

Notable support is $23.00, $27.30, and $30.60 per share.

Notable resistance is $37.50, $46.00, and $60.00 per share.

Street Assessment

Analysts on a consensus basis have high expectations for the company going forward.

Growth Est | AIG | Industry | Sector | S&P 500 |

Current Qtr. | -113.40% | -99.90% | -93.80% | 9.50% |

Next Qtr. | -48.50% | -99.80% | -92.70% | 15.30% |

This Year | 266.70% | 99.80% | 23.30% | 7.20% |

Next Year | -6.70% | 20.80% | 6.90% | 13.10% |

Past 5 Years (per annum) | -42.91% | N/A | N/A | N/A |

Next 5 Years (per annum) | 21.93% | 13.20% | 10.60% | 8.72% |

Price/Earnings (avg. for comparison categories) | 9.41 | 19.56 | 13.83 | 14.69 |

PEG Ratio (avg. for comparison categories) | 0.43 | 1.67 | 0.95 | 1.41 |

Source: Table and data from Yahoo Finance

Analysts have high expectations, as analysts on a consensus basis have a 5-year average growth rate forecast of 21.93% (based on the above table). This growth rate is above the industry average for next 5-years (13.20%).

Earnings History | 11-Dec | 12-Mar | 12-Jun | 12-Sep |

EPS Est | 0.63 | 1.12 | 0.57 | 0.86 |

EPS Actual | 0.82 | 1.65 | 1.06 | 1 |

Difference | 0.19 | 0.53 | 0.49 | 0.14 |

Surprise % | 30.20% | 47.30% | 86.00% | 16.30% |

Source: Table and data from Yahoo Finance

The average surprise percentage is 44% above analyst forecast earnings over the past four quarters (based on the above table).

Forecast and History AIG Insurance

Year | Basic EPS | P/E Multiple |

2003 | $ 3.10 | 21.38 |

2004 | $ 3.77 | 17.42 |

2005 | $ 4.03 | 16.93 |

2006 | $ 5.38 | 13.32 |

2007 | $ 2.40 | 24.29 |

2008 | $ (37.84) | - |

2009 | $ (93.69) | - |

2010 | $ 14.75 | 3.27 |

2011 | $ 8.60 | 2.7 |

2012 | $ 3.74 | 9.41 |

Source: Table created by Alex Cho, data from shareholder annual report

The EPS figure shows that throughout the 2003-2006 period earnings were growing due to favorable economic conditions. Then the company was adversely affected by the great recession throughout 2007-2009, as the net income rapidly declined, and AIG eventually logged the biggest loss in corporate history. During 2010 the company was able to generate a profit by restructuring the company; this involved selling business units, which inflated earnings by $17.7 billion dollars. Once the United States economy exited the recession in 2010-2012 the company earnings have improved, albeit gradually. In 2011 the abnormal earnings of $8.60 were due to a provisional benefit from taxes worth $18.03 billion dollars. The improvements in net income for 2010-2011 were one-time events and should not be considered a part of the long-term earnings growth trend. So in essence, 2012 is likely to be the most normal year for AIG over the past 5 years.

Source: Table created by Alex Cho, data from shareholder annual report

By observing the chart we can conclude that the business is somewhat cyclical and is affected by macroeconomics. Therefore one of the largest risk factors to AIG is the slowing of international gross domestic product growth. So as long as the global economy continues to grow, the company will generate reasonable returns over a 5-year time span based on the forecast below.

AIG Stock Prices Forecast Next 5 Year

Source: Forecast and table by Alex Cho

By 2018 I anticipate the company to generate $10.19 in earnings per share. This is because of earnings growth, improving global outlook, earnings management and continued development overseas.

The forecast is proprietary, and below is a non-linear chart indicating the price of the stock over the next 5-years.

AIG Stock Chart Forecast Next 5 Year

|

| AIG Stock Chart Forecast Next 5 Year |

Source: Forecast and chart by Alex Cho

Below is a price chart incorporating the past 10 years and the next 6 years. Detailing 16 years in pricing based on my forecast and price history on December 31st of each year.

Source: Forecast and chart created by Alex Cho, data from shareholder annual report, and price history is from Yahoo Finance.

*The period 2003-2008 were price quotes based on pre-split stock prices (multiply by 20 to accurately calculate the price of the shares between 2003 and 2008). On 7/01/2009 the stock had a 1:20 split (reverse split).

Investment Strategy AIG Insurance

AIG currently trades at $35.20. I have a price forecast of $37.94 for 2013. AIG is in a long-term up-trend. I anticipate momentum in the price of the stock, as the growth rate offers compelling stock appreciation for the foreseeable future.

Short Term

Over the next twelve months, the stock is likely to appreciate from $35.20 to $38.60 per share. This implies 9.6% upside from current levels. The technical analysis indicates an up-trend (break above the symmetrical triangle formation). While the previously mentioned price forecast using fundamental analysis further supports the trade set-up.

Investors should buy AIG at $35.20 and sell at $38.60 to pocket short-term gains of 9.6% in 2013. This return is pretty measly, meaning that short-term investors would likely do better investing in other opportunities.

Long Term

The company is a great investment for the long-term. I anticipate AIG to deliver upon the price and earnings forecast despite the risk factors (macroeconomic, competition, etc.). AIG's primary upside catalyst is international development, and earnings management. I anticipate the company to deliver upon my forecasted price target of $100.12 by 2018. This implies a return of 185% by 2018. This rate of return is exceptional, considering AIG has a market capitalization of $52B. The extra liquidity makes this a compelling growth investment for institutional investors who require higher liquidity.

Conclusion buy AIG Stock

Buy AIG on long-term growth. AIG has not died off the surface of the earth; it is more stubborn than a roach. The conclusion remains simple: buy AIG.

Articel copyright by Alex cho - published by seekingalpha.com

tag ; aig insurance stock prices forecast 2013, aig stock 2014, aig stock 2015, aig insurance stock 2016, aig investment strategy 2013, aig insurance stock technical analysis 2013-18, aig stock prices forecast 2013-2014, aig shares prices forecast next 5 year, AIG Common Stock, par value, aig company exspected 2013

Zack China Life Insurance stock rating prices target $49.00

Best Insurance Stock - China Life Insurance stock rating prices target $49.00 : Zacks reiterated their neutral rating on shares of China Life Insurance (NYSE: LFC) in a research report sent to investors on Friday morning. The firm currently has a $49.00 price target on the stock.

Zacks’ analyst wrote, “China Life reported a net loss in the third quarter, due to a surge in operating expenses, which offset the operating income increases. However, premiums earned and investment income witnessed a notable improvement. Total assets and shareholders’ equity also improved, while cash fund deteriorated. Meanwhile, the subordinated debt issue has improved solvency ratio.

Extensive domestic distribution channel, strong investment and stable ratings are other positives. However, the constant decline in operating cash flow is affecting financials. The company also inherently faces substantial interest rate and currency risks, which limit the upside. Despite a strong brand name, significant competition on the domestic front hampers earnings growth. Overall, we expect limited upside in the near term.”

Shares of China Life Insurance traded down 0.43% during mid-day trading on Friday, hitting $46.16. China Life Insurance has a 52 week low of $33.00 and a 52 week high of $47.39. The company has a market cap of $84.896 billion and a P/E ratio of 60.60.

What the Palins found underneath the Christmas tree yesterday

Todd:

Washcloths and condoms

Sarah:

Red Bull, some fashion sense

Bristol

Dancing lessons, a man

Willow

hairbrush

Piper

an education

Trig

Parents who love him

Tripp

soap to wash out his mouth with, quality time with his daddy

Washcloths and condoms

Sarah:

Red Bull, some fashion sense

Bristol

Dancing lessons, a man

Willow

hairbrush

Piper

an education

Trig

Parents who love him

Tripp

soap to wash out his mouth with, quality time with his daddy

Health insurance rate review authority by Montana State

Best insurance stock option today - Review Authority Health Insurance Rate : Despite changes in federal regulations, health-care costs are still a concern for most Montanans. However, legislation proposed for this coming Montana legislative session could help ensure that all Montanans will at least be treated fairly by insurance companies looking to increase their rates.

The legislation, House Bill 87, which is being promoted by Montana State Auditor Monica Lindeen and sponsored by Rep. Jeff Welborn, R-Dillon, will give Lindeen’s office review authority for insurance rate increases. This might seem to be a minor issue, but Montana is only one of three states that currently have no authority to review insurance rate increases, Lindeen said.

As state auditor, Lindeen has the authority to review insurance rates in all other categories includ-ing home, auto and life. This has allowed her to reduce rate increases that have seemed too unjusti-fiably high.

It also allows her to make sure rate increases are legal, said Lindeen spokesman Lucas Hamilton.

The lack of review authority also gives insurance companies the ability to take advantage of Mon-tanans. Lindeen sites a recent example where a health insurance company proposed rate increases around the country. The average increase was 18 percent, but in some cases customers saw their rates increase by 50 percent.

These rates were challenged by Montana’s neighbor South Dakota, which has health insurance rate review authority. South Dakota negotiated a lower rate increase with this particular insurance company on behalf of its citizens. Montana wasn’t allowed the same benefit and customers of that particular insurance company were forced to accept the rate increases with no discussion.

Another benefit to the rate review authority is that it benefits the health insurance industry as a whole in Montana by bringing fairness to the marketplace. Lindeen will have the authority to review rates that are too low and attempt to undercut the market, said Blue Cross and Blue Shield of Montana spokesman Fred Cote.

Without state review authority, insurance companies could run rates much lower than the market standard, upsetting the balance in the market and also running the risk of becoming insolvent, Cote said.

For the health insurance industry it will provide an independent review of rates, which will help consumers ensure the increases are justified, he said. This is a bill that Cote said Blue Cross and Blue Shield will support.

The federal government, through the Affordable Care Act, also has health insurance rate review authority when rates increase by at least 10 percent. However, the local review authority is a better option for Montanans because local regulators will better understand local markets.

During the 2011 legislative session, a similar bill was tabled in the House Business and Labor Committee after a compromise was reached between the auditor’s office and a handful of Montana health insurance companies along with the Montana Chamber of Commerce and the Montana Small Business Alliance. Mysteriously, this commonsense bipartisan legislation was a casualty of the opposi-tion to President Barack Obama’s Affordable Care Act.

HB 87 represents the same compromised bill from the last session. Let’s hope this time around legislators can see the benefits for Montanans and give the state auditor the review authority her office needs.

Source : http://helenair.com

Hiscox insurance Stocks outlook 2013

Best Insurance Stock - Hiscox insurance Stocks outlook 2013 : Hiscox estimates Sandy net claims of approximately £90 millio n for the impact of sandy, international specialist insurer Hiscox has today announced an estimate for the impact of Superstorm Sandy. Although considerable uncertainties still exist around the impact of Superstorm Sandy, the insurer said that based on an insured market loss of $20bn, it estimates net claims of approximately £90m. Superstorm Sandy hit parts of North America and Canada in October causing destruction of buildings and infrastructure. Twice a year Hiscox publishes its expected losses for modelled catastrophes including exposure to US windstorm. The insurer stated that the estimate was within the published range, and was within Hiscox's overall budgeted loss expectations for the year.

Key Statistics for HSX

| Current P/E Ratio (ttm) | 7.7493 |

|---|---|

| Estimated P/E(12/2012) | 10.5669 |

| Relative P/E vs. UKX | 0.5056 |

| Earnings Per Share (GBP) (ttm) | 0.6013 |

| Est. EPS (GBP) (12/2012) | 0.4410 |

| Est. PEG Ratio | 0.1110 |

| Market Cap (M GBP) | 1,837.35 |

| Shares Outstanding (M) | 394.28 |

| 30 Day Average Volume | 333,287 |

| Price/Book (mrq) | 1.3739 |

| Price/Sale (ttm) | 1.4734 |

| Dividend Indicated Gross Yield | 3.84% |

| Cash Dividend (GBp) | 6.0000 |

| Last Dividend | 08/08/2012 |

| 5 Year Dividend Growth | 10.23% |

| Next Earnings Announcement | 02/25/2013 |

About Hiscox Insurance Company Inc.

The company was formerly known as American Live Stock Insurance Company, Inc. and changed its name to Hiscox Insurance Company Inc. in December 2007. The company was founded in 1952 and is based in Geneva, Illinois. Hiscox Insurance Company Inc. operates as a subsidiary of Hiscox, Ltd.

416 South 2nd Street Geneva, IL 60134

United States Founded in 1952

Phone: 630-232-2100

Fax: 630-232-2292

www.amlivestock.com

Subscribe to:

Comments (Atom)